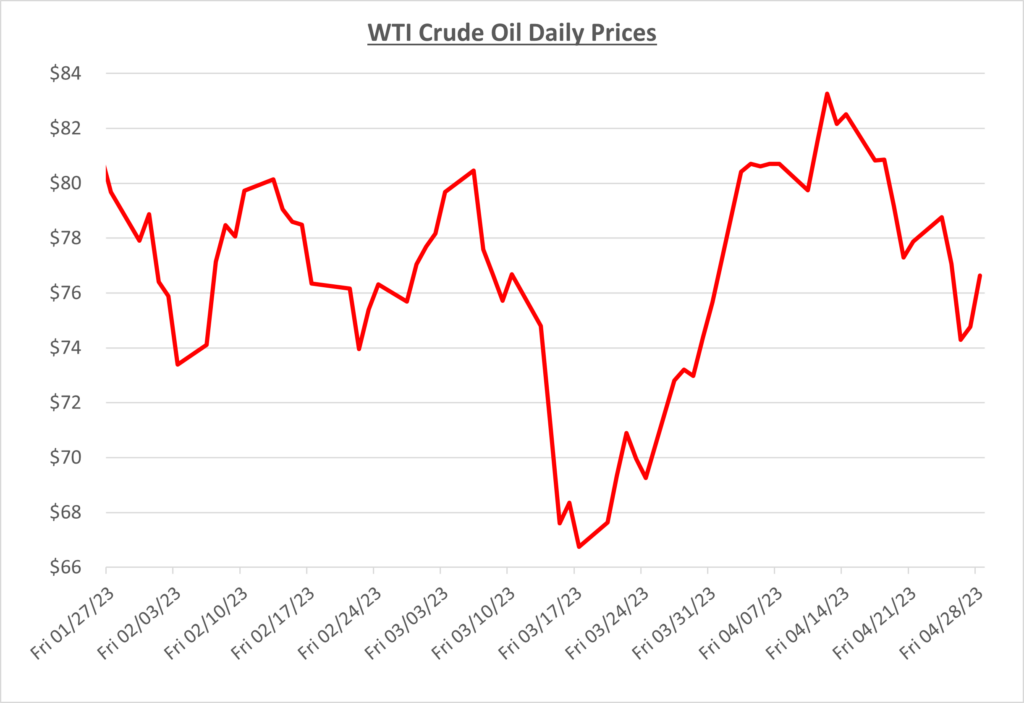

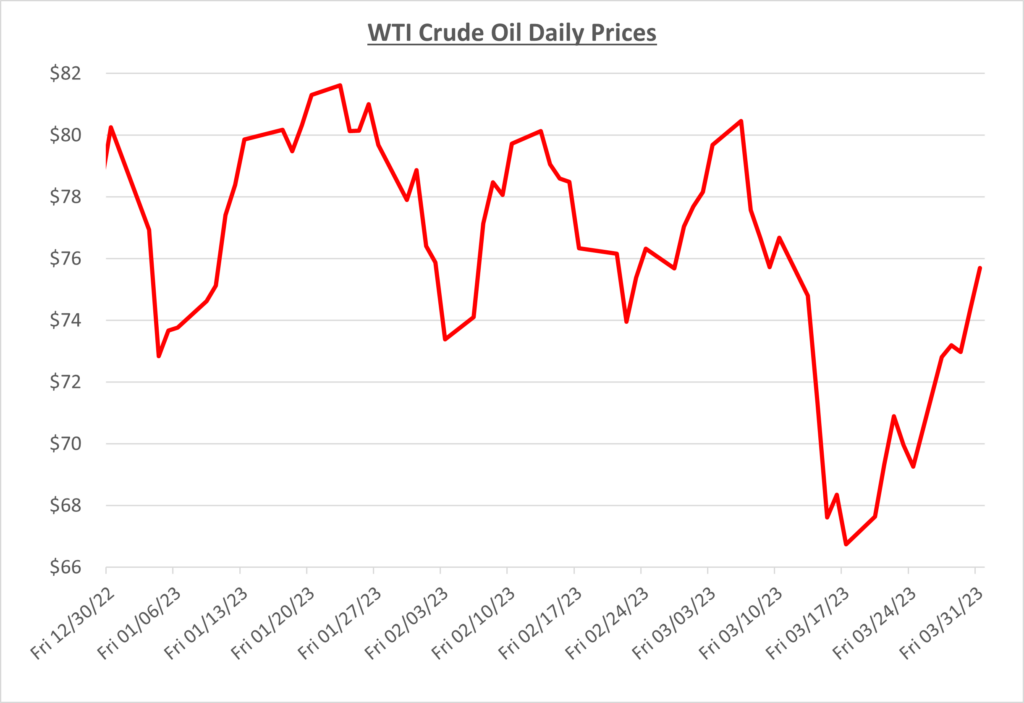

Early in March, oil prices continued their upward trend from the end of February, briefly topping $80/barrel. The main factor was the belief that global demand was rising with China’s economy rebounding. Aiding that further, was some positive news about the U.S. economy as inflation fears were cast aside for the time being. The following graph shows the daily price movements over the past three months:

As we continued further into March, oil prices dropped drastically due to the failures of Silicon Valley Bank (SVB) and Signature Bank. The U.S. government was forced to step in and stop the bleeding. SVB, the 16th largest lender in America, caught energy traders by surprise and caused concern that this could have a ripple effect with other banks. There was at least one more bank woe globally with Credit Suisse until they were bought by rival UBS Group. Oil prices fell as low as $66/barrel, the lowest seen since December of 2021.

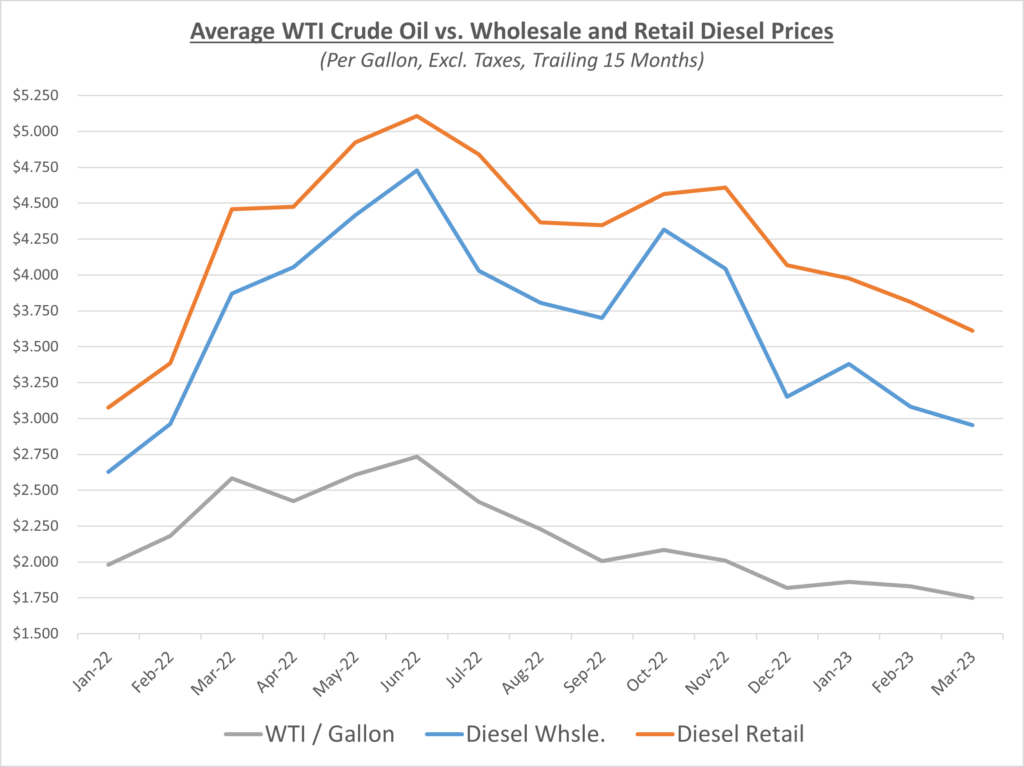

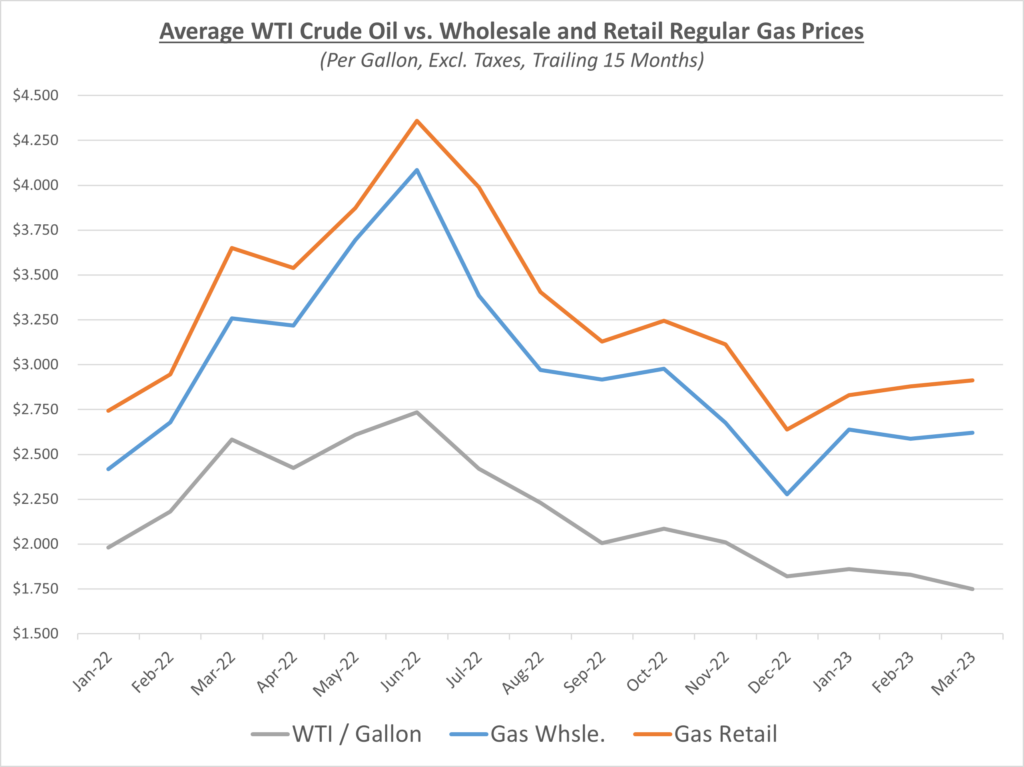

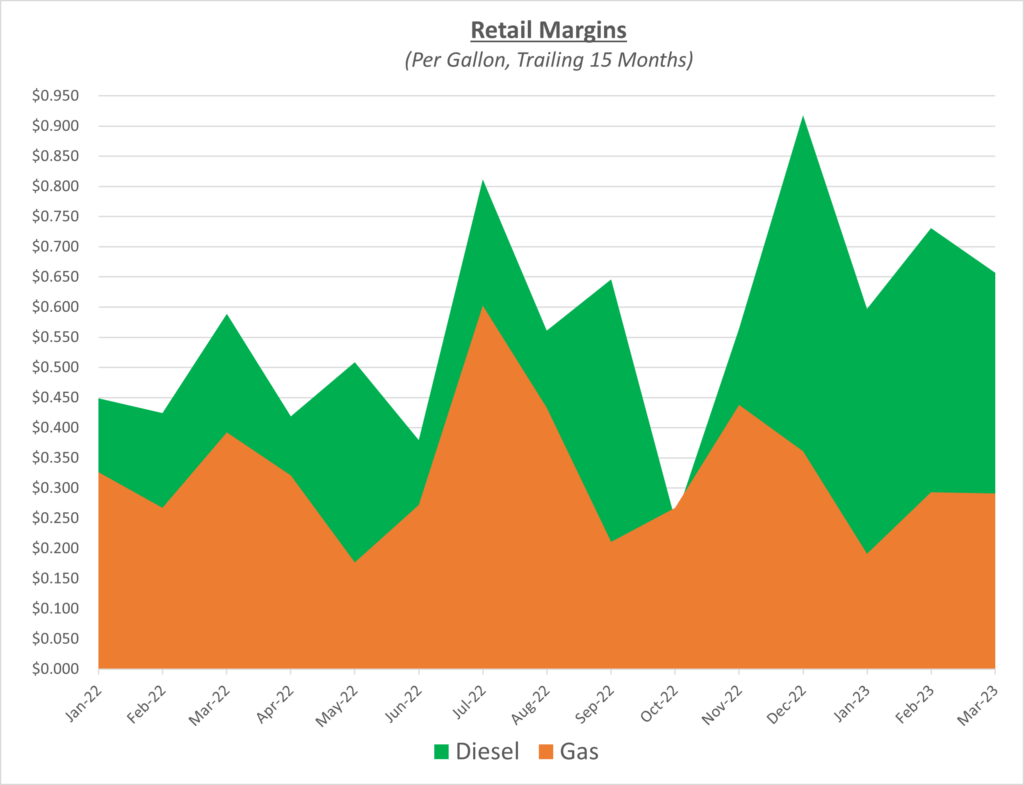

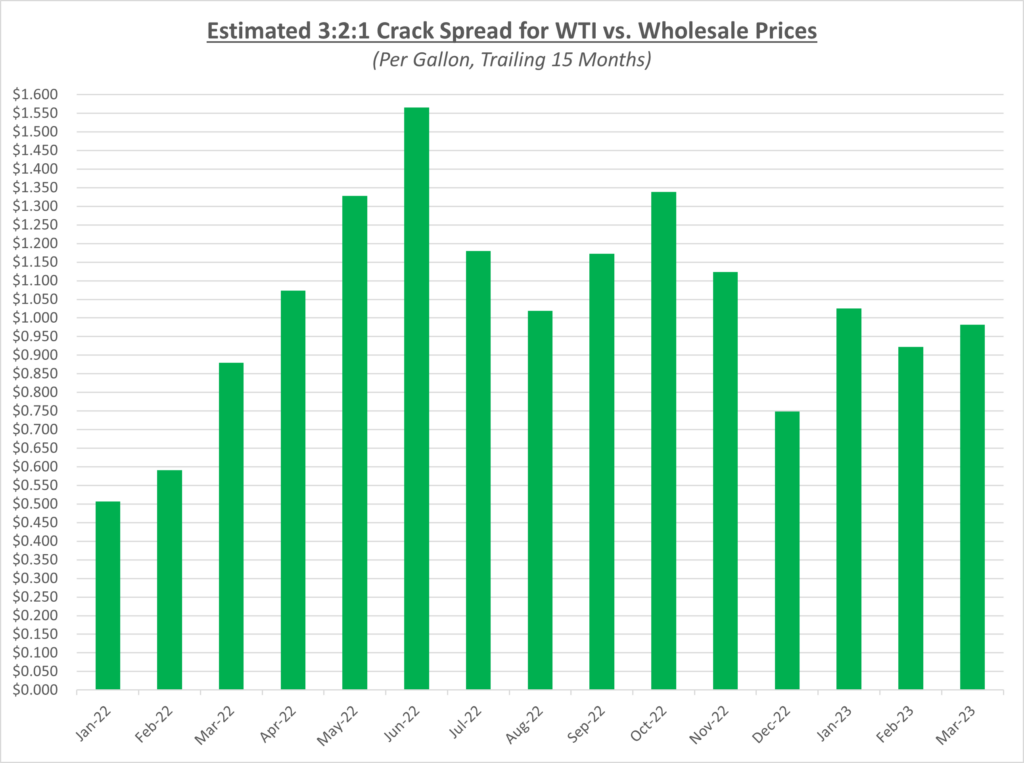

The graphs below show the movement of crude oil (converted to gallons) along with wholesale and retail fuel prices over the trailing 15 months:

Diesel wholesale and retail prices fell steadily in March. Typically, when wholesale prices are falling, retail does not follow as quickly, helping to keep margins high. However, margins were so high in February that there was a slight decline. Wholesale gas and retail prices headed the opposite way of diesel, trending slightly higher. Gas margins were flat from February to March. The following graph shows the retail margins over the trailing 15 months:

Crack spreads rose from February into March and remain above average. Retailers are still waiting for these glory days to end as predicted by many. So far, they’re not as high as seen in 2022, but have still been profitable for retailers year to date.

After starting the month high and then falling with the bank failures mid-month, oil prices are trending upward yet again beyond $80/barrel. According to AAA, the national average gas prices increased by roughly $0.12 to $3.51/gallon compared to last month. The national average diesel price decreased by about $0.18/gallon to about $4.20/gallon.

The factors that were keeping oil prices from rising the past month or two (sufficient supply, lukewarm winter, a slow-moving Chinese economy, and fears of a recession) seems to be reversing and causing oil prices to spike. We’re now entering spring and demand seems to be increasing in both the U.S. and globally. Supply seems to be getting tighter with a pipeline shutdown in Iraq and OPEC+ announcing they will reduce production starting in May through the rest of 2023. The cuts are estimated to be an additional 1.16 million barrels per day. Finally, the fear of further banks failing has also eased for now.

Sokolis believes that oil prices will remain in the $75-90/barrel range but could go higher with further supply disruptions. We will do our best to keep you updated with the latest news.